Film Tracking or How I Learned to Stop Worrying and Love Opening Weekends

Colin Whitlow

How do we track movie performance?

In a late summer Deadline article, Anita Busch wrote about the recent poor performance of movie tracking services and laments the studios’ wasted money spent on wildly inaccurate box office projections. Ms. Busch is not alone in highlighting this issue – in recent months reporters for many industry publications have written articles bemoaning the state of the so-called “predictive reports.” In her article, Anita cites an industry insider who thinks “[the tracking services] need to go a little deeper in their research, in the way that they ask and who they ask.” According to the article, some blame the tracking services for not being able to keep up with the habits and influencers of a generation of consumers making nearly constant use of smart phones and social networks in deciding how to spend their time. While the commonly used tracking services have used focus groups to understand consumer behavior for decades, they’re less savvy at taking into account online behavior. Ms. Busch notes that the focus of tracking companies should be on accurately representing projects’ profitability, since that’s what most stakeholders are concerned with after all. She closes the article with a question: “So how do you fix it? Anyone?”

[I am eagerly raising my hand – this slows down my typing but I’m hoping sooner or later they’ll call on me]

Focusing on overall profitability sounds like an excellent idea! But before deciding how to fix a system that may or may not be broken, let’s take a moment to consider what these companies are trying to do and how they arise at their projections…

The purpose of these services’ reporting is to provide a snapshot of the marketplace and how specific marketing materials are being received at the current time. They attempt to do this primarily by polling groups of likely moviegoers (on phone, web and in person), asking whether they’re "aware" of specific movies and to report on the likelihood they will see it. These respondents are broken into quadrants: males <25, males >25, females <25, and females >25, with racial divisors sometimes incorporated. These are relatively broad dividing factors, but as such they serve as flexible indicators of awareness of many types of films and film releases. In addition to weekly reports, many of these firms offer bespoke services like testing trailers, TV spots and print ads, conducting exit polls, hosting recruited-audience screenings, organizing focus groups, testing titles and positioning and studying franchises. However, it is the weekly reports that are purchased in large numbers and used to project opening weekend returns – projections responsible for the recent bad press when widely off the mark.

Boiling it down, these weekly tracking reports are trying to determine 2 things: (1) the number of people aware of upcoming movies; and (2) how many of them intend to buy tickets at the theater. Using polling to study the success of a film’s marketing campaign probably feels worth the investment to most of the studios and production companies that subscribe to it. However, the questions are whether these reports should be used as predictive indicators and whether they, along with actual box office reporting, need be the only metric for film investors to value types of films.

Those of us who take an interest in such things want a larger selection of touchpoints to gauge film performance. We want to be able to place films in a clear context so not every film is being judged on the same scale. Investors in small films don’t expect anywhere near the level of return that a studio blockbuster commands. Yet, in broad strokes, the industry and media look at next weekend’s box office as though all the films are running in the same race. It’s wrong to act like we can gauge all films against one another in a single list. But more than that, this lack of sophisticated reporting and predictive metrics is detrimental to the film industry by making it appear even more volatile than it actually is.

When do we track movie performance?

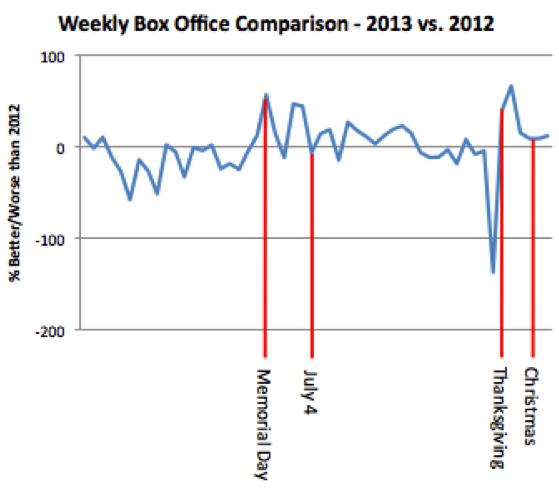

These reports highlight the industry obsession over the all-important opening weekend. Why do we put so much emphasis on a film’s performance during opening weekend? Because we do, that’s why. Sure, one can examine how over time, the industry has matured in a way that it has naturally come to focus on opening weekend because it’s a relatively straightforward way for distributors and exhibitors to cull poorer performing films from a finite number of movie theaters. There’s nothing wrong with that per se – the industry has to create some Darwinian mechanism to allow specific films to survive and perish in the theatrical window and opening weekend has risen to become a key indicator. But does such an overwhelming focus on the first three days actually make sense in a world where a film’s revenue is earned over such a longer period and through so many other avenues than just theatrical exhibition?

The book publishing industry, which itself is in the midst of some much needed renovation, uses the term frontlist to mean current titles – books that were released recently and which are still receiving conscious marketing resources. Backlist refers to anything that doesn’t fit that category. While many publishers do focus on frontlist to drive the bulk of their revenue, an increasing number of companies rely equally if not more so on maintaining a backlist that performs strongly for years. By achieving stable sales from a sizable backlist library, these companies feel comfortable when taking measured risks on the frontlist they believe in rather than nervous over the success or failure of each new title.

The analogy between film and publishing isn’t exact, but if you were to draw a line between film and publishing release cycles, frontlist would be equivalent to the theatrical window (assuming a typical release pattern). Backlist would be the windows after a film is in theaters (VOD, DVD, etc.). Studios don’t need to be taught the lesson of how important “backlist” revenue is to their bottom line. The money made from film libraries dating back nearly a century continue to bolster studio revenues and require much less servicing than the heavily marketed premiere of their next film. However, in part because of the sheer size of many film budgets, they continue to place enormous emphasis on the film that’s premiering rather than focus on extending the active lifespan of past releases.

We do sometimes read articles reporting on aggregate film sales, especially as films cross their next $100mm threshold or meet some other notable milestone. However, the focus on a film’s performance wane week over week as it ages. For the consumer or hobbyist reader, this is likely the way it should be – popular film journalism should be entertaining so it should focus on what is new. However, film investors need the ability to continually view a film in its proper context, throughout its life, to understand how it’s performing compared to expectations, what those expectations were, how other correlated films are performing at that time, etc.

The film finance index is being designed to provide just that type of context. Not to replace tracking services. Not to diminish the importance of opening weekends. But to add a tool to an investor’s toolbox that provides clarity about the performance metrics they’re seeing. In my next blog post I’ll delve into my latest progress toward this end.